Mortgage interest rates dropped below 3% this past week with an average interest rate of 2.97% on a 30-year fixed-rate mortgage according to the Freddie Mac Primary Mortgage Market Survey. As the chart below shows, mortgage interest rates have not been below 3% since February 25, 2021 when they also averaged 2.97%. Rates are still up from the record low rate of 2.65% in January, but as you can see on the chart, are still at a rate that is historically low!

Now is the time to buy or perhaps refinance your existing mortgage.

Anyone that has been thinking of buying a home should, if able, shift into high geat and find one now to take advantage of the low rates and the increased buying power that comes with it. The first step would be to get yourself pre-approved and, for that, I would recommend Michael McCarthy with Flat Branch Home Loans…he’s great and our firm does a lot of business with him. You can find his info at STLBestLender.com. If you a homeowner with a mortgage and no plans to move, I would also suggest you get in touch with Mike to see how much money you can save by refinancing your existing mortgage at a lower rate.

LendingTree just released a list of the 50 large metro areas with the most competitive housing markets in the U.S. on which St Louis was ranked as the 6th most competitive market. This list was based upon LendingTree’s assessment of the quality of the buyer’s in each market, based upon their strength as a buyer from a financing standpoint.

So, while not an analysis of which cities have the most buyers showing up at a listing or where listings are receiving the highest number of offers, it’s about the quality of the home buyer’s from a competitive standpoint. This makes sense, as today the hard part isn’t necessarily finding a buyer for a new listing, it’s about the listing agent analyzing the offers and helping the seller determine not only which may have the best terms, but which buyer has the best ability to perform. After all, having a great offer doesn’t really mean anything if the deal doesn’t close.

Most Competitive Housing Markets

(click on table for complete list)

In analyzing the quality of the buyer’s and assessing the competitiveness of each market, LendingTree took into consideration the following for each metro area:

The share of home buyers shopping for a mortgage even before they found the house they wanted. This is indicative of a good buyer that wants to be prepared to react quick and understands the importance of being pre-approved to be make their offer more attractive to the seller.

The average down payment percentage. A buyer with a larger downpayment is going to look like a stronger buyer to a seller.

Percentage of buyers have have good credit (above a 680 credit score). Better credit means more financing options and lower cost financing which can enable the buyer to pay more than someone with lower credit and have the same monthly cost in terms of payment. A better credit score also means there is a better chance of the deal closing.

A good buyer’s agent will know everything above and help their client through the process to make them have the best chance possible of getting their offer accepted. Likewise, a good listing agent will know how to scrutinize buyer’s and help their seller client pick the one that not only has offered an acceptable price and terms but has the highest likelihood of closing. For a recommendation of a great St Louis buyer’s agent or listing agent, contact me.

The St Louis real estate market has started off 2021 strong, but is a change coming? Closings of home sales in January were strong with more sales closing than in January of last year, but with everything going and the uncertainty of the economy will it continue? I address both the current state of the St Louis real estate market, as well as discuss our “leading indicator” data which gives us a glimpse of where the market is headed in the St Louis Real Estate Market Update video you can access below.

[xyz-ips snippet=”Market-Update-Video-Package”]

[xyz-ips snippet=”Seller-Resources—Listing-Targeted”]

Last week, the Federal Housing Finance Agency (FHFA)announced that effective January 1s, 2021, the maximum loan amounts for Fannie Mae and Freddie Mac conforming loans will be increased from $510,400 to $548,250. Once a home buyers loan amount exceeds the Fannie and Freddie limits, their loan is considered a “jumbo” loan and typically less attractive terms, so an increase in the Fannie and Freddie limits is definitely helpful to home buyers in higher price ranges.

Fannie Mae and Freddie Mac are also increasing the loan limits for loans to purchase multi-family properties as well. The multi-family property limits for 2021 are:

Fannie Mae issued their monthly housing forecast for April which includes, among other data, a forecast of what mortgage interest rates will be in the coming months. Last months forecast had projected that mortgage rates would continue to decline moving forward but only to a low of 3.1% before the end of 2021 while the April forecast predicted the interest rate on a 30-year fixed-rate mortgage would fall to 2.9% in the 2nd quarter of 2021 and stay there through the balance of the year.

If you’re able, now’s the time to buy!

While the effects of the COVID-19 pandemic, such as job loss, is going to take some would-be home buyers out of the market, for those that are still able to buy, now is a great time to buy a home. There are many factors that play in favor of buyers today, such as the fact that there are about 1/3 fewer of them (buyers in the market) now than this time last year, sellers that want to have fewer people coming through their homes and interest rates. As our chart below shows, not only are rates low now, they are projected to go much lower even.

Why not wait until next year when the rates hit their lowest?

Good question, but there are several reasons not to wait. First off, the rates shown on my chart are “projections”, or to put it another way “an educated guess”, so there is no guarantee rates will actually come down as predicted. In addition, once the stay at home orders go away and we start moving back to something closer to normal, I anticipate there will be a flood of buyers to the market which, along with lower interest rates (if that happens) will likely drive home prices up. So, for buyers that are able, they may get a better buy today, with less competition, still get a good interest rate and then if rates do fall as predicted can easily refinance to take advantage of lower rates.

As a result of the COVID-19 National Emergency Servicing and Loss Mitigation Program declared by President Trump, the U.S. Department of Housing and Urban Development (HUD) sent a letter yesterday to its loan servicers making them aware of new COVID-19 National Emergency Loss Mitigation Options. HUD told the lenders that the new options for borrowers go into effect immediately but the lender must implement them no later than April 30, 2020.

The Mortgagee (lender) must not deny COVID-19 National Emergency Home Retention Options to Borrowers that experience an adverse impact on their ability to make on-time Mortgage Payments due to the COVID-19 National Emergency and satisfy the loss mitigation criteria set forth in this section.

(A) Forbearance for Borrowers Affected by the COVID-19

National Emergency If a Borrower is experiencing a financial hardship negatively impacting their ability to make on-time Mortgage Payments due to the COVID-19 National Emergency and makes a request for a forbearance, the Mortgagee must offer the Borrower a forbearance, which allows for one or more periods of reduced or suspended payments without specific terms of repayment.

The initial forbearance period may be up to 6 months. If needed, an additional forbearance period of up to 6 months may be requested by the Borrower and must be approved by the Mortgagee.

The term of either the initial or the extended forbearance may be

shortened at the Borrower’s request

.

(B) COVID-19 National Emergency Standalone Partial Claim

The Mortgagee must waive all Late Charges, fees, and penalties, if any, as long as the Borrower is on a Forbearance Plan.

For any homeowners with an FHA loan that are struggling to make their house payments, they should contact their loan servicer to see if they are eligible for relief under this plan.

The typical median-priced existing home sold for $233,000 in February 2019 and a year later, as the chart below shows, in February 2020 the typical median-priced home sold for $235,000, an increase of just under 1%. Here’s the beauty though, thanks to interest rates dropping from an average of 4.41% a year ago to 3.29% today, even with the slight increase in price, the typical St Charles County home costs less today than a year ago! Not just by a little either as the payment on the median price a year ago (no money down) would have been $1,178.18 at the current rates at the time, the payment today, at the higher price but lower rates would be just $1,019.15, a savings of $159.03/month or 13.5%! Oh, and just to show the “compound effect” of this, over the life of the loan, you will save $55,249 in interest.

Mortgage interest rates hit a record low this week with an average interest rate of 3.29% on a 30-year fixed-rate mortgage according to the Freddie Mac Primary Mortgage Market Survey. As the chart below shows, interest rates came close to this level at the end of 2012 but then quickly shot up to over 4.5% shortly after.

Now is the time to buy or at least refinance!

Anyone that has been thinking of buying a home should, if able, shift into high geat and find one now to take advantage of the low rates and the increased buying power that comes with it. The first step would be to get yourself pre-approved and, for that, I would recommend Michael McCarthy with Flat Branch Home Loans…he’s great and our firm does a lot of business with him. You can find his info at STLBestLender.com. If you a homeowner with a mortgage and no plans to move, I would also suggest you get in touch with Mike to see how much money you can save by refinancing your existing mortgage at a lower rate.

For quite a while now we have enjoyed the positive effects on the real estate market from low mortgage rates but it looks like it’s going to get even better! Yesterday’s announcement by the Fed of the emergency step of lowering the benchmark U.S. interest rate by one-half of one percent, in an effort to offset the negative effect tot eh financial markets from the coronavirus will likely lead to even lower mortgage interest rates.

What’s the connection between the federal funds rate and mortgage interest rates? This is something often asked not only by homebuyers but is even within the real estate community as since the Federal Reserve doesn’t “set” mortgage rates, the connection is not always clear. I’m not an expert in this area by no means, but I have a decent understanding of it and will share it from the perspective of the most popular home mortgage, the 30-year fixed-rate mortgage. First, we have to understand where the money for those mortgages comes from. It comes from investors, investors that compare an investment in 30-year mortgages to other comparable investments. One of those comparable investments would be the 30-year treasury.

As you may have noticed, I’ve been pretty optimistic about the outlook for the real estate market this year however, that is not always the case as I call it like I see it. The reason for my optimism is based upon what a true data geek like myself would base it upon, data! So, what’s the data that has me believing 2020 will be a good year for the housing market in St Louis and beyond? Several things:

As I have been reporting here for the past couple of years now, mortgage delinquency and foreclosure rates have continued to decline which show the strength of the economy as a whole as well as the housing industry.

As the US Economic Indicators charts below show, since peaking around 2010, the unemployment rate, 30-year mortgage rate and mortgage delinquency rates have all steadily declines to either record lows or at least the lowest rate in recent history.

As the St Louis unemployment, home prices and rent chart below shows, unemployment in St Louis has fallen to the lowest level in decades and the relationship between home prices and rents show home prices lagging behind rents indicating that we’ll likely see continued, good housing appreciation rates.

As the 30-year fixed rate mortgage chart below shows, mortgage rates are at near record low rates giving buyers much more buying power. In my market update video I shared here a day or two ago I illustrate just how much more buying power this translates into.

As I reported last week, St Louis home sales last year managed to top the prior year slightly, in spite of the low-inventory market we have been stuck in. This shows the demand that is out there.

As I reported earlier this week, the home sales trend for 2020 in St Louis is in positive territory has well.

The maximum loan amount for an FHA-Insured home loan on January 1, 2020, will increase from $314.827 to $331,760 for a single-family home purchased in the St Louis metro area. FHA insured home loans have lower credit standards than a typical conventional loan, require a downpayment of just 3.5% and allow all of the purchasers closing costs to be paid by the seller (up to a limit) thereby extending the opportunity of homeownership to a wider audience.

Below are all of the FHA Mortgage Limits for the St Louis MSA for 2020:

One-Family dwellings – $331,760

Two-Family dwellings – $424,800

Three-Family dwellings – $513,450

Four-Family dwellings – $638,100

To find out more about FHA home loans, or to get pre-approved for an FHA home loan click on the button below to connect with Mike McCarthy.

The good news just keeps coming for the residential real estate industry! The most recent is from a report just released by CoreLogic showing the mortgage delinquency rate in the U.S. was at 3.8%, the lowest rate in at least 20 years! In addition, not one state in the country had an increase in overall delinquency rates in September.

Foreclosure Inventory Reaches Low as well…

The foreclosure inventory rate for September was 0.4%, another 20+ year low!

In August, the overall mortgage delinquency rate (30 or more days past due) was 3.7% for the U.S. which is a 0.2 percentage point decline from a year ago and is the lowest overall delinquency rate in 14-years, according to date just released by CoreLogic. The delinquency rate for August of 3.7% marks the lowest delinquency rate during the month of August in 20 years. The serious delinquency rate (120+ days late) decline of 1.2% a year ago to just 1.0% in August 2019, nearly a record low. The Foreclosure Rate fell in August 2019 to 0.4% from 0.5% a year ago.

Missouri mortgage delinquency rates are low as well…

During August 2019, the overall mortgage delinquency rate for Missouri was exactly the same as the national rate, 3.7%. The serious delinquency rate in Missouri was 1.1%, just slightly above the national rate, and the foreclosure rate was 0.2%, half of the national rate.

The St Louis real estate market trends remain steady and consistent! The St Louis home sales and price trends give me an optimistic outlook for next year. Low-interest rates continue to offset some of the cost of the increases in home prices that have occurred. Find out more, as well as get information on some of St Louis’s best resources for home buyers and sellers in our just-released market update video.

After mortgage interest rates on a 30-year fixed rate mortgage nearly hit 5 percent back in November, they have steadily declined and this past week fell to an average of 4.37% according to the Freddie Mac Primary Mortgage Market Survey. Last weeks 30-year fixed rate mortgage rate of 4.37% was the lowest average rate report by the survey since Feb 8, 2018, when the average rates were 4.32%.

The outlook for mortgage interest rates looks promising as well with the most recent Fannie Mae Housing Forecast predicting the 30-year fixed rate will stay at 4.5% through the end of 2020.

The overall mortgage delinquency rate in the U.S. fell in August to the lowest level in over 12 years, according to a report just released by CoreLogic. According to the report, 4.2% of all St Louis home mortgages were 30+ days delinquent in August 2018, a decline of over 14% from a year ago when the rate was 4.9%. During the same period, seriously delinquent mortgages, those that are 90+ days late, in St Louis dropped from 1.8% a year ago to 1.4% in August 2018, according to the report.

The Mortgage Bankers Association (MBA), in their Mortgage Finance Forecast released this week predicted that interest rates on home mortgages will continue to rise this year and will hit 5% early next year. According to the report, the interest rate on a 30-year fixed rate mortgage is expected to come in at an average of 4.6% for the 3rd quarter, which just ended and then rise to an average of 4.9% during the last quarter of this year. Interest rates are then forecast to hit 5.0% during the 1st quarter of 2019, rise to 5.1% by the second quarter, then stay around 5.1% through the end of 2020, according to the report.

Today, Freddie Mac, through their Primary Mortgage Market Survey® revealed that for the current average interest rate on a 30-year fixed-rate mortgage is at 4.52%. which is just a slight decline from a week ago when the rate was 4.53% and the same as the week before that. After 30-year fixed-rate mortgages hit 4.66%, the highest rate in 7-years, back in late May, they have been trending downward a little, which is good news for the real estate market!

30 Year Fixed Rate Mortgage Average – 2000 – Present

Mortgage interest rates have been on the rise and hit their highest level in seven years toward the end of May, however, the higher rates don’t appear to be having an effect on the number of people in St Louis obtaining home loans yet. The table below is based upon the latest data from ATTOM Data Research, just released yesterday, and shows that there were 6,830 home purchase mortgage loans obtained in the St Louis metro area during the 1st quarter of this year. This represents an increase of nearly 10% from the number of home purchase mortgage loans that were obtained in St Louis a year ago. Even if we go back to the first quarter of 2016, when the average 30-year fixed rate mortgage rate was below 4%, there were just 6,093 home purchase loan originations, 12.1% fewer than the most recent quarter.

The number of St Louis homeowners refinancing their home mortgages during the first quarter of this year dropped over 10% from a year ago and was down over 15% from the first quarter of 2016.

There is a lot of activity in the St Louis real estate market! The inventory of homes for sale in St Louis remains low, interest rates have dropped a little over the past couple of weeks, home prices are beginning to soften as we move beyond the peak spring market and demand is still strong.

Freddie Mac has been tracking average mortgage rates since 1971 through their Primary Mortgage Market Survey® and yesterday it revealed that, as the chart below shows, the average interest rate on a 30-year fixed-rate mortgage was at 4.6%, the highest rate in over 7 years. The last time mortgage interest rates were this high was back on May 5, 2011 when the 30-year rate hit 4.71%.

Even with the recent increase, mortgage interest rates are still reasonably low from a historical perspective. As the second chart below illustrates, 20 years ago the rates were around 8 percent. Mortgage interest rates then spent nearly a decade around the 5% – 6% range before beginning the descent after the housing bubble burst in 2008.

(We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

New home construction in the St Louis area is off to a good start for 2018 with a total of 326 building permits for new homes being issued during January for the 7-county St Louis area reported on by the Home Builders Association of Eastern Missouri. This permit activity in January represents an 11% increase over the activity in January 2017 when there were 293 new home permits issued. During the month of January 2018, 4 of 7 counties saw an increase in building permits from January 2017 (Jefferson County +26%, Franklin County +143%, Warren County +1%, St Louis City +371%) while the remaining 3 saw declines (St Louis County -25%, St Charles County -10%, Lincoln County -29%).

It takes more than a month for a trend…

Just like I often comment with regard to home prices and sales, looking at a single month of activity really does not paint the whole picture and, while it may be a good “leading-indicator” of where things are headed, it’s not going to accurately depict a trend. For this, I believe looking at the past 12-month period and comparing it to the prior 12-month period is more accurate. It takes into account the seasonal fluctuations that occur and adjust for unseasonal weather during a given month that could skew the data if just looking at a one-month period. The table belows the total building permits for the 12-month period ending January 31, 2018 and comparies that activity to the prior 12-month period for each of the 7-counties reported on. As you can see, five of the counties have a double-digit increase in new home building permits issued from the prior 12-month period while St Charles County shows a double-digit decline, and Lincoln County a slight decline.

(We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

New Home Building Permits- St Louis Area – January 2018

The St Louis real estate market typically hits its peak during the spring months then continues strong into summer. Come August, the housing market in St Louis tends to slow as families squeeze in vacations and school begins. After Labor Day we normally see an increase in activity until the market goes into something reminiscent of hibernation for the Thanksgiving and Christmas season.

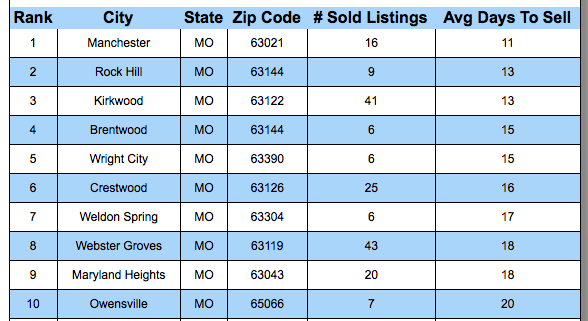

Even though Labor Day is just a few days away, home sales that closed within the past 30 days show that homes are still selling quickly in St Louis. Below is our list of the 10 St Louis cities where homes sold the fastest in the past 30 days. As the list reveals, the city of Manchester, where homes that sold did so in a median time of only 11 days, came in at number 1 on the list and the median time to sell was only 15.5 days for the cities on the top 10 list.

St Louis Fastest Sold Cities

(click on table for complete and up to date information)

According to a report just released by Corelogic, the 30-59 day mortgage delinquency rate in March (the most recent month reported) fell to just 1.7%, the lowest level since January 2000. The “seriously delinquency” rate (30+ days late) fell to 4.4% in March, the lowest level sine November 2007, according to Corelogic.

In addition, the “transition rates” all improved as well from a year ago. Transition rates show which way the borrowers are moving, from slightly delinquent to more delinquent, or from slightly delinquent to current for example. Below are the transition rates for March 2017, according to the Corelogic report:

Borrowers going from current to 30 days late – 0.6% for March 2017, down from 0.7% in March 2016

Borrowers going from 30 days late to 60 days late – 11.6% for March 2017, down from 13.2% in March 2016

Borrowers going from 60 days late to 90 days late – 20.8% for March 2017, down from 23.1% in March 2016

All of this is good news for the real estate industry as the trends are positive and are is a good “leading indicator” of what is to come. As mortgage delinquencies decrease, foreclosures, short sales and other distressed home sales decline, putting less downward pricing pressure on the housing market and providing sustainability to the improving housing market.

Speaking of mortgages, if you are considering refinancing, want to know what current rates and terms are, or would like to get pre-approved for a mortgage, I would highly recommend speaking with Ryan Derryberry, a mortgage loan professional with Movement Mortgage. Ryan is a great guy, is honest and knows his stuff. Movement is a great company, founded and operated on great principals and offer some mortgage products you won’t find anywhere else….More information on Ryan, including his contact info, can be found here.

(We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

Mortgage Delinquency rates, borrowers that are 60 or more days past due, are projected to be 2.21 percent for the 4th quarter of 2016, down from 2.46% the quarter before and marking the 13th consecutive quarter mortgage delinquency rates have fallen, according to a report just released by TransUnion. According to the report, mortgage delinquency rates peaked at 7.21 percent during the 1st quarter of 2010 and have declined for 23 of the last 26 quarters since. TransUnion considers the current mortgage delinquency rate to be normal and is projecting the delinquency rate will fall even further next year down to 2.11% by the end of 2017.

(We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

According to the Freddie Mac Primary Mortgage Market Survey (PMMS) released yesterday for the past week, interest rates on a 30-year fixed rate mortgage increased 5 basis points (1/20th of 1%) to 4.13 percent , the highest rate they have been at during 2016. Last year at this time the PMMS showed average interest rates at 3.95 percent so, while rates have increased over the past year, the amount has been fairly small.

However, mortgage interest rates are being forecasted by many economists and industry guru’s to hit 4.5% – 5.0% during 2017. While we’ve seen predictions like that for a couple of years in a row now, I think it’s going to come true this time therefore, if you have been thinking about buying, you may want to start looking now!

(We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

New mortgage applications for a home purchase declined last week 7.0 percent from the prior week, according to a report just released by the Mortgage Banker’s Association (MBA). The MBA’s Market Composite Index, which is how they track the volume of loan applications, fell to it’s lowest level for home loans for a purchase since January 2016.

Interest rates decline as well…

While the number of loan applications declined, so did the interest rate on home mortgages, according to the MBA report:

30 year fix rate conventional mortgages decreased to 3.71 percent from 3.73 the week before,

30 year fixed rate jumbo loans (larger than $417,000) decreased to 3.71 percent from 3.72 percent the week before,

FHA loans bucked the trend with interest rates increasing to 3.56 percent from 3.54 percent the week before,

5/1 ARMS decreased to 2.93 percent from 2.97 percent.

St Louis home sales increase 5 percent during the same period:

The tables below reflect St Louis home sales for the same one-week period, compared with prior week, as in the MBA’s report and illustrate that St Louis perhaps appears to be bucking the trend. St Louis saw an increase in home sales during the most recent week, which, theoretically, should translate into an increase in home mortgage applications, contrary to what we see in the MBA report on a national basis.

(We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

Over the past 5 years or so I have written a few articles on the topic of the mortgage interest deduction (MID) and how, in spite of what many others in the industry say, I didn’t think it was that critical to the housing industry. All the while, the National Association of REALTORS (NAR) (of which I’m proud to be a member, just happen to disagree on this topic) has staunchly supported the MID and warned that if the deduction went away the housing market and home buyers would suffer. NAR published a fact sheet on the topic stating:

Repealing the Mortgage Interest Deduction (MID) is a form of tax increase. Families with children would bear more than half of the total increase.

IRS data show that taxpayers in the 35-45 age group take the largest MID on average compared to any other age group of taxpayers.

First time home buyers would be hurt the most if the MID is curtailed.

Current data from the IRS show that 65% of the taxpayers who have claimed the MID made less than $100,000.

The housing market has not emerged from the crisis that began in 2007.

(We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

Mortgage interest rates have been falling since last Thursday when the referendum passed for the United Kingdom to exit the European Union. As the chart below shows, interest rates on a 30 year fixed-rate mortgage today averaged 3.44%, a new 52-week low and a decline of nearly 3/4 of 1 percent from a year ago when they were 4.20%. The payment on a $160,000 home loan at today’s rates would be $713 (principal and interest), a decline of nearly 9 percent from a year ago when the payment on the same loan amount would have been $782. (We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

A recent article by STL Today indicated that home affordability in St Louis had fallen, specifically noting that affordability in St Louis County had fallen below historic “norms”. As is always the case with stats, it depends upon which data you are taking into account and the accuracy of the data. I decided to take a look at the data and see if my data showed the same result as the STL Today article.

Affordability is UP in St Louis county, not DOWN…

As the table below shows, home affordability in St Louis county has actually increasedin the past year, not decreased as reported in the aforementioned article. For the purposes of my analysis, I used home sales data for “non-distressed” sales only, so not including foreclosures or short sales, to get a more accurate picture of the true market.

Affordability has improved in Jefferson County as well but, as the table below shows, has declined in the past year in the city of St Louis, Franklin county and St Charles county. (We work hard on this and sure would appreciate a “Like”)[iframe http://www.facebook.com/plugins/like.php?href=https%3A%2F%2Fwww.facebook.com%2FStLouisRealEstateNews&send=false&layout=standard&width=50&show_faces=false&font&colorscheme=light&action=like&height=35&appId=537283152977556 100 35 ]

Missouri Online Real Estate, Inc. 3636 South Geyer Road - Suite 100, St Louis, MO 63127 314-414-6000 - Licensed Real Estate Broker in Missouri

The owner and authors this site are providing the information on this web site for general informational purposes only and make no representations, warranties (expressed or implied) or guarantees of any kind whatsoever, as to the accuracy or completeness of any information on this site or of any information found by following any link on this site. Furthermore, the owner and authors of this site will not be liable in any manner whatsoever for any errors or omissions in information on this site, nor for the availability of this information. Additionally the owner and authors of this site will not be liable for for any losses, injuries or damages in any way from the display or use of this information or as the result of following external links displayed on this site, or by responding to advertisements displayed, or contained, on this site

In using this site, users acknowledge and agree that the information on this site does not constitute the provision of legal advice, tax advice, accounting services, investment advice, or professional consulting of any kind nor should it be construed as such. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal, or other competent advisers. Before making any decision or taking any action on this information, you should consult a qualified professional adviser to whom you have provided all of the facts applicable to your particular situation or question. None of the tax information on this web site is intended to be used nor can it be used by any taxpayer, for the purpose of avoiding penalties that may be imposed on the taxpayer.

All of the information on this site is provided as is, with no assurance or guarantee of completeness, accuracy, or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability, and fitness for a particular purpose.

This site contains external links to other sites not owned or controlled by the owner of this site, therefore the owner of this site does not control or guarantee in any manner the accuracy or relevancy of any information obtained through following such links. Links contained on this site are for users convenience and users should exercise extreme caution when following links. Including a link on this site does not constitute an endorsement of the site linked to or any views or opinions expressed on the site, products or services offered on outside sites or the companies or organizations that own and operate outside sites.

This site may accept payment for advertising, for displaying advertisements, through affiliate relationships with companies or may receive referral fees or commissions from companies as a result of recommending or referring people to a website. This site may also accept free product samples, free services, gift cards or cash to review a product or service. All paid and sponsored content may not always be identified as such. Any product claim, quote or other representation about a product or service should be verified with the manufacturer or provider.

")