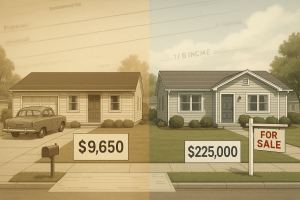

Buried in a 1961 Sunday Post-Dispatch Newspaper, an ad by Income Investment Co. promised St. Louisans a new home for a price “everyone” could afford—$9,650 with just $350 down and a principal-and-interest payment of $54.31. The 3-bedroom ranches in Eureka’s brand-new “Shaw’s Garden” subdivision even came with five king-size closets and concrete streets. Chrysler’s Fenton plant was ramping up a few miles away, and the ad all but wrote the script for the blue-collar American Dream.

Fast-forward to 2025. That $9,650 price tag converts to roughly $99,000 in today’s dollars using the CPI, yet recent sales on the same streets: Hill, Weber and Butler, are closing around $225,000. In other words, every original dollar turned into about $2.25 of real value, beating inflation by more than double.

But the monthly payment story paints an even clearer picture. In 1961, that $54 house payment represented about one-ninth of a typical household’s income. Today, even with Eureka’s median income above six figures, a similar slab ranch pushes that burden to around one-sixth. That’s a 26% increase in how much of the paycheck goes to just principal and interest.

And it’s not just about mortgage interest rates. Even if mortgage rates dropped a full percentage point tomorrow, payments on a $225,000 home would still eat up about 14% of median income, well above the 11% level from 1961. The core issue is simple: home prices grew about 23 times since then, while incomes only rose about 19 times.

In St. Louis, that’s playing out visibly in neighborhoods like Eureka, where a ranch listed at or below $250k might look like a bargain. But once you run the math, those “starter” homes are putting more pressure on buyers than they did 60 years ago. Taxes, insurance and HOA fees only stack the load higher.

So how did a modest 1,200 square-foot ranch on a 60×125 lot beat the broader economy? It wasn’t upgrades or architecture…it was land, location, and scarcity. Back then it was Chrysler; today it’s Amazon’s hub, I-44 logistics, and a top school district. Even with remote work more common, homes near job corridors still carry value, just not as heavily as they once did.

And this isn’t just true in Eureka: throughout the St. Louis metro area, plenty of communities still attract first-time buyers and value-focused shoppers looking for affordable homes in convenient locations with decent schools—places like Affton, Maplewood, Fenton, Maryland Heights, University City, St. Ann, St. Charles, and Pacific, to name a few.

Key takeaways for 2025:

- “Affordable” doesn’t mean easy: Even plain homes under $250k are stretching buyers more than they did 60 years ago.

- Lot size and location still carry weight: For many buyers, a dated ranch with a real yard beats out newer builds crammed onto tight lots in weaker locations.

- Location still matters: Whether it’s getting to work, shopping, restaurants, ballgames, or just cutting down drive time—access and convenience still add value.

- Equity builds fast if you bought early: A $9,650 house in 1961 might be worth $225k+ now—and likely with six figures of tax-free gain for homeowners. The model still works.

- Perspective for today’s buyer: $54/month sounded great in 1961—but it also fit the paycheck. Today’s buyer has a different income and a different hurdle. The trick is knowing where the long-term upside still lives.

Thinking of selling a home you’ve owned forever? Or trying to make sense of today’s prices as a buyer or investor? Let’s run the numbers.

Reach out to MORE, REALTORS® today and put some data behind your next move.

1961 Vintage Ad for New Homes in Eureka