Seller financing is one of those ideas that tends to get dismissed quickly. For many homeowners, the reaction is immediate. It sounds complicated. It feels uncertain. And in some cases, it raises concerns about what could go wrong if a buyer does not follow through. But like many things in real estate, the perception and the reality are not always the same.

What Seller Financing Actually Means

Seller financing simply means the seller acts as the lender.

Instead of receiving the full purchase price at closing from a bank-funded loan, the seller allows the buyer to make payments over time based on agreed terms. Those terms typically include a down payment, an interest rate, and a defined repayment schedule.

While it may feel unconventional, the structure itself is well-established and has been used in various markets for decades.

Where the “Risk” Conversation Comes From

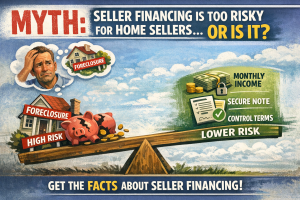

The concern most sellers have is straightforward. What happens if the buyer stops making payments? That is a valid question. Any time payments are made over time, there is some level of risk involved. The key difference with seller financing is that the seller is not giving up control in the same way as a traditional sale.

The seller holds the note and maintains a secured interest in the property. If structured properly, there are legal remedies available if the buyer defaults. That process can take time and may involve legal costs, which is why upfront structuring and buyer qualification matter.

What Often Gets Overlooked

One of the most overlooked aspects of seller financing is how much control the seller retains in the process. Unlike a traditional lender, a seller can:

Set qualification standards for the buyer

Require a meaningful down payment

Establish terms that reflect the level of risk they are comfortable with

In many cases, sellers are able to evaluate a buyer more holistically than a standard underwriting model would allow. Many sellers also choose to use third-party loan servicing companies to handle payment collection and documentation, reducing the day-to-day involvement.

Why Some Sellers Are Considering It Again

This approach is most commonly considered when a property is owned free and clear or when existing financing allows for it. In periods where interest rates are elevated or lending standards are tighter, financing becomes one of the biggest obstacles for buyers. That creates an opportunity. Offering seller financing can: expand the pool of potential buyers, make a property more competitive without adjusting price, or create flexibility in how a deal is structured.

For some sellers, it is not about taking on unnecessary risk. It is about solving a problem that exists in the current market.

The Income Component

Another factor that is often overlooked is the income potential. Instead of receiving all proceeds at closing, a seller who finances the purchase may receive monthly payments that include interest. Depending on how the terms are structured, this can create a predictable income stream over time. For sellers who do not need immediate access to all of their equity, this can be an alternative way to think about the value of the asset.

Where It Does Not Make Sense

Seller financing is not a fit for every situation. It may not be ideal for sellers who need full liquidity immediately, prefer a clean break from the property or are not comfortable managing or overseeing a loan, even with third-party servicing. Like any strategy, it works best when it aligns with the seller’s goals and timeline.

A More Balanced View

The idea that seller financing is “too risky” often comes from focusing on what could go wrong without considering how the structure can be designed to manage, though not eliminate, that risk.

In practice, many of the same principles that apply to traditional lending still apply here. Due diligence, clear terms, and proper documentation all play a role in how successful the arrangement will be. Most listings will never use this strategy. But the ones that do are often the ones that needed a different approach to get to the finish line.

Seller financing is not a new concept, and it is not inherently risky or inherently safe. It is simply a different way to structure a transaction. For the right seller, in the right situation, it can open doors that a traditional approach may not.

Karen Moeller

STLKaren.com

Karen.McNeill@STLRE.com

314.678.7866

About the Author:

Karen Moeller is a St. Louis area REALTOR® with MORE, REALTORS® and a regular contributor to St. Louis Real Estate News, helping clients make informed, data-driven decisions.