A buyer finds a home with a 3% assumable mortgage and immediately starts doing the math. At today’s interest rates, the monthly payment difference can look enormous. Suddenly, a house that may have felt financially out of reach starts seeming possible again.

Then comes the part many buyers do not expect: the low interest rate may be assumable, but the seller’s equity usually is not. For many buyers, that is the moment the excitement changes.

In a market where affordability has become one of the biggest obstacles facing buyers, low-rate assumable loans have started attracting attention that they rarely received during years of cheap borrowing. The phrase “assumable mortgage” now appears in listing descriptions with increasing frequency, often positioned almost like a premium feature. And in some cases, it genuinely can be.

In simple terms, an assumable mortgage allows a qualified buyer to take over an existing loan, including its interest rate and remaining repayment terms. FHA, VA, and some USDA loans are often assumable, while most conventional loans are not. A buyer assuming a 3% mortgage instead of obtaining new financing at a much higher rate could potentially save hundreds of dollars per month in payment costs. That is the part people hear about most often.

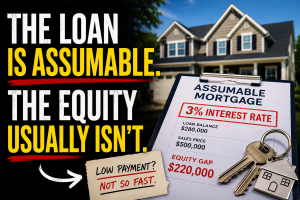

What receives far less attention is the equity gap. Assuming a mortgage does not mean assuming the entire purchase price of the home. It usually means taking over only the seller’s remaining loan balance. If the property has appreciated significantly since the seller purchased it, the buyer must still bridge the difference between the loan balance and the current sale price.

That gap can become substantial surprisingly quickly. A seller may have a remaining mortgage balance of $280,000 on a home now selling for $500,000. Even if the buyer successfully assumes the low-rate mortgage, there may still be more than $200,000 that must be covered through cash, secondary financing, or some combination of the two. A buyer may discover that while the monthly payment looks incredibly attractive, coming up with the additional cash needed to bridge the equity gap is a completely different challenge.

That is where many assumable mortgage conversations become more complicated than buyers initially expect. On paper, assumable mortgages can look like shortcuts around higher interest rates. In practice, they often shift the challenge from monthly payment affordability to upfront cash requirements and transaction complexity.

The process itself can also be more involved than many buyers realize. Borrowers generally must still qualify with the lender overseeing the assumption. Credit, income, debt ratios, and underwriting standards still matter. Assumptions can also take longer to process than traditional financing, creating additional timing considerations for both buyers and sellers.

VA loans can introduce another layer of complexity involving entitlement eligibility. In some situations, a seller’s VA entitlement may remain tied to the property unless certain conditions are met during the assumption process. While these situations can often be navigated successfully, they add another reason assumable mortgages are rarely as simple as they initially sound.

None of this means assumable mortgages are a bad option. In the right situation, they can create meaningful savings and open opportunities that might otherwise not exist in a higher-rate environment. For some buyers, particularly those with significant cash reserves or strong equity from a previous sale, an assumable mortgage can be an extremely valuable financial tool.

But the structure is often more nuanced than headlines and social media posts make it appear. Buyers often hear phrases like “take over a 3% mortgage” and understandably assume the transaction works much like stepping into the seller’s full financial position. In reality, the low interest rate is only one piece of a much larger equation involving equity, financing structure, qualification standards, and timing.

And in many cases, the larger the gap between current market value and the remaining loan balance, the more difficult the assumption becomes for the average buyer. That is especially true in markets where home values have risen rapidly over the past several years.

For sellers, assumable mortgages can absolutely attract attention and generate interest from buyers searching for alternatives to today’s borrowing costs. But they do not automatically simplify a transaction, and they do not eliminate the financial realities surrounding equity and qualification.

Like many things in real estate, assumable mortgages are neither miracle solutions nor meaningless gimmicks. They are legitimate financial tools, but in today’s housing market, low interest rates have become valuable enough that buyers are no longer just shopping for homes. In some cases, they are shopping for the mortgage attached to them.

Karen Moeller

STLKaren.com

Karen.McNeill@STLRE.com

314.678.7866

About the Author:

Karen Moeller is a St. Louis area REALTOR® with MORE, REALTORS® and a regular contributor to St. Louis Real Estate News, helping clients make informed, data-driven decisions.