After over 40 years in the real estate business in St Louis I’ve seen many times just how fast a good, or even great housing market can turn sour as well as the other way around. Two years ago, economic conditions relevant to the housing market included:

A St Louis housing market that is showing signs of slowing as well as concern and even fear among real estate agents and consumers.

Does this mean St Louis home prices will come crashing down?

First off, I’m not an economist, in fact I didn’t even attend college and I certainly don’t have a crystal ball showing me the future, but I am a data junkie that has lived through a variety of markets spanning more than 4 decades. My experience as well as my study of past markets as well as current indicators of things to come certainly give me an opinion. In times past, my opinions on the market have been spot on, almost to the point that I even surprised myself (such as in October 2006, at the peak of the housing boom when I predicted the collapse) and other times I’ve been wrong, sometimes way wrong. The reality is that the housing market is affected, or can be affected by so many different economic factors, as well as social issues, consumer sentiment and more that I don’t believe anyone can predict what it’s going to do accurately consistently.

The bond market had one of the worst days in history yesterday resulting in mortgage interest rates on a 30-year fixed rate mortgage hitting 6.0% and above. This is the highest rates have been since November 20, 2008 when the mortgage interest rates were 6.04%, according to Freddie Mac’s Primary Mortgage Market Survey®.

Is there a silver-lining to the higher interest rates?

Given that the reason for the higher interest rates has to do with our high inflation rates and declining economic conditions, it’s hard to find much positive to say about what is happening. Having said that, the one thing that comes to mind is these rate increases will no doubt slow down the rapid price growth on homes we’ve seen over the past couple of years. This will likely cause home prices to flatten and the premiums buyers have paid over and above what the buyer, seller and agents involved knew the home was actually worth are history in my opinion.

So, while as a buyer, you will be facing higher interest rates than you would have a year ago, you should receive some relief in the price not being as high as it would have if the low rates were still here, less competition due to some buyers leaving the market and being able to purchase a home without paying a significant premium above the value to get it.

Every month Fannie Mae surveys consumers to gauge their sentiment toward whether its a good time to buy or sell a home and publishes the result in their Home Purchase Sentiment Index® (HPSI). In the most recent HPSI report, 79% of the people surveyed said they felt now was a bad time to buy a home, which is the highest percentage of people feeling this way since the survey was begun in 2012. Seventeen percent of those surveyed felt it was a good time to buy a home and 4% didn’t know whether it was or not.

There were 2.71 million home loan originations during the first quarter of this year in the U.S., according to the U.S. Residential Property Mortgage Origination Report from ATTOM. This is an 18% decline from the prior quarter, the largest quarterly decline since 2017 and marks the fourth straight quarterly decline in loan originations according to the report.

Refinancing saw a bigger decline than home purchases…

During the first quarter of this year there were 1,446,622 loans originated that were refinances of existing mortgages which is a decline of 21.7% from the prior quarter. There were 1,011,975 loans originated for home purchases during the quarter and this was down 18.3% from the prior quarter.

St Louis is the metro that saw the second-highest decline…

I according to the report the metro area with the largest quarterly decrees and loan origination’s for home purchases was Huntsville Alabama with a 61.3% decrease followed by St Louis Missouri with a 55.3% decrease.

On May 12th the 30-year fixed rate mortgage interest rate hit 5.3%, the highest rates since June 2009, according to Freddie Mac’s Primary Mortgage Market Survey®. As the chart below illustrates, mortgage interest rate have declined the last three consecutive weeks falling to 5.09% at the end of last week, the lowest rate since April 14th when the average interest rate was 5.0%.

On May 12th the 30-year fixed rate mortgage interest rate hit 5.3%, the highest rates since June 2009, according to Freddie Mac’s Primary Mortgage Market Survey®. As the chart below illustrates, mortgage interest rate have declined the last two consecutive weeks falling to 5.10% yesterday, the lowest rate since April 28th.

There are more affordable options…

The chart I selected to show below also shows the mortgage interest rates for 15-year mortgages as well as something almost no one has had a reason to talk about for several years, adjustable rate mortgages (ARM’s). With mortgage interest rates as low as they were, ARM’s were rarely considered by a purchaser however, today they provide a more affordable option than a 30-year fixed mortgage. For example, the 5/1 arm shown on the chart below had a rate of 4.2% yesterday.

There have been a lot of reports over the past month about rising interest rates (mortgage rates on a 30-year fixed-rate mortgage hit 5.27% last week) as well as rising inflation rates (8.5% in March) and the effect these things will have on the housing market. It’s no doubt they will have some affect on home prices and sales and I have been watching the data on St Louis home prices and sales closely and so far there does not appear to be much impact.

St Louis home sales increase in April from March…

There are two ways we analyze home sales at MORE, REALTORS®; the traditional manner, which is what almost all public reports are based upon, closed sales (which are really indicative of what the market was like 1-2 months previously since that is when the contracts were typically written) and then by use of our STL Real Estate Trends Report, which gives us a better idea of the current activity. Our trends report shows the number of new contracts written on listings, so current sales activity as well as the number of new listings entering the market. The good news is, when looking at St Louis home sales activity for April, both closed sales and newly written contracts increased from the month before.

As our chart below shows, there were 2,134 homes sold in St Louis (5-county core market) during April, a 6.4% increase from March when there were 2,005 homes sold. As the STL Real Estate Trends Report shows, there were 3,279 new contracts written on homes during April in the St Louis 5-county core market, an increase of 5% from the prior month when there were 3,124 contracts written.

In an article published yesterday, I referenced the Sitzer vs National Association of REALTORS law suit and said I would have a more in-depth discussion about that suit and here it is. The lawsuit was filed by Joshua Sitzer, Amy Winger, Scott and Rhonda Burnett and Ryan Hendrickson on June 21, 2019 against the National Association of REALTORS® and the parent companies of major real estate companies and franchises including Coldwell Banker, ReMax, Keller Williams and Berkshire Hathaway Homeservices.

The Sitzer lawsuit was filed in the United States District Court for the Western District of Missouri sought to be certified as a class action lawsuit on behalf of “all persons and entities who listed properties on one of four Multiple Listing Services…and paid a broker commission from at least April 29, 2015 until the Present…“. The four MLS’s listed in the suit that this applies to are:

Heartland MLS (Kansas City, MO)

MARIS MLS (St Louis, MO)

Southern Missouri Regional MLS (Springfield, MO)

CBOR MLS (Columbia, MO)

Last Friday, April 22, 2022, Stephen R. Bough, a Federal Judge for in the Western District of Missouri, issued an order granting the class action status for the lawsuit the Plaintiffs sought.

The past several days have not been good for the National Association of REALTORS® (NAR) from a legal perspective at least.

First, last Friday, April 22, 2022, Stephen R. Bough, a Federal Judge for in the Western District of Missouri, certified a lawsuit against NAR as a class action suit.The suit, known as the “Sitzer” suit as the original plaintiffs were Joshua Sitzer and Amy Winger, alleges that the defendant, the National Association of REALTORS® “created and implemented anticompetitive rules which require home sellers to pay commission to the broker representing the home buyer“. The plaintiffs in the suit also allege that the other defendants, which include Realogy Holdings Corp, Homeservices of America, Inc., Re/MAX LLC and Keller Williams Realty, Inc., “enforce those rules through anticompetitive practices.” I believe this action by the court was expected and likely did not come as a surprise to anyone but it was not good news for NAR or the other defendants. In the coming days I’ll be doing an in-depth article on this one.

Then, yesterday, the United States Court of Appeals for the 9th Circuit delivered another and this time, a likely unexpected, blow to the National Association of REALTORS® in the form of a reversal of a suit against NAR that had been dismissed previously by a lower court. The suit, PLS.com v. the National Association of REALTORS®, is another suit alleging anti-trust violations by NAR and the other defendants which are all MLS’s. The suit was brought originally by PLS.com as a result of NAR enacting its “Clear Cooperation Policy” which for all intents and purposes, dictates to agents and brokers how and when they can market their listings. I’ve written several articles specifically on this policy in the past which can be found using the following links:

The Missouri Department of Commerce and Insurance (DCI) is the state agency that investigates complaints against insurance companies made by consumers in Missouri. Annually, the DCI releases its complaint report reporting on the complaints made in the preceding year by company, type of insurance, etc. In compiling the report the DCI assigns a “complaint index” to each company, based upon the number of complaints the department received for a consecutive three-year period relative to the amount of product-specific premium a Missouri licensed company experienced that same period. An index number of 100 means that the department received the normally expected number of complaints about that company, an index number less than 100 indicates the company was the subject of less than the normally expected number of complaints and an index that is greater than 100 shows the department received more than the normally expected number of complaints about that company.

Below, I have compiled a list of the top 20 providers of homeowners insurance in Missouri (based upon market share) ranked by their complaint index with the companies with the worst complaint index first. The companies list with a red background have a complaint index above 100 and the ones in green have a complaint index below 100. As the table shows, Auto Club Family Insurance Company as the worst complaint index on the list at 166, followed by Allstate Vehicle and Property Insurance Company (145), Auto Owners (131), Travelers (121) and State Farm (117) rounds out the top 5 with the worst complaint indexes.

To obtain the complete report showing all companies as well as complaint indexes for all lines of business click here or on the table below.

This week it was announced that the U.S. inflation rate in March had increased to a staggering 8.5%the highest rate in over 40 years as illustrated by the chart below. The last time the inflation rate was higher than this was in December 1981 when it hit 8.9%. The “inflation rate” that I’m referring to, and is the most commonly reported, is based upon the Consumer Price Index for All Urban Consumers (CPI-U): U. S. city average. One of the categories included in the CPI-U is “shelter”. The report shows the shelter inflation rate at 5% which, on the surface sounds low however, the median price of homes sold in St Louis in March was $250,000 an increase of just over 4% from March 2021 when the median sold price was $240,000.

What does an inflation rate of 8.5% mean for the real estate market?

With everything going on in our economy, country and world now I think it’s literally impossible to predict what is going to happen on any front with any level of accuracy however, a good guide would be what has happened in the past during similar times. With this in mind, lets look at what the market looked like the last time inflation was at this level, December 1981:

Mortgage interest-rates on a 30-year fixed mortgage were an average of 17%-18% (see chart below)

The inflation rate actually reached a peak of 14.4% in March of 1980

St Louis home prices peaked during the 1st quarter of 1979 then declined until bottoming-out during the 2nd quarter of 1981 (see chart at bottom)

Yesterday, I shared that, according to the Fannie Mae Home Purchase Sentiment Index (HPSI), nearly three-fourths of consumers think now is not a good time to buy a home. However, the same survey that produced that data also showed that tw0-thirds of the consumers that responded said if they would buy a home vs rent if they were in fact going to move. As our chart below illustrates, for 3 of the last four months, 66% indicated they would buy. While the percentage that indicated they would buy was as high as 72% last May, it was in fact the same, at 66% a year ago in March as well as the year before that in March. So, while consumers don’t think now is a good time to buy, it appears many are doing it or would do it, anyway.

Every month Fannie Mae surveys consumers about owning and renting a home as well as about other issues related to the housing market and economy and from the results publishes its Home Purchase Sentiment Index (HPSI). One of the components of the index is what the sentiment is on whether now is a good time to buy a home or sell a home. In April 2022, HPSI consumers’ sentiment on whether now is a good time to buy a home hit an all-time low with just 24% of respondents saying now is a good time to buy a home. As the charts below illustrate, 73% of respondents said now was a bad time to buy a home.

Some remodeling projects are done by homeowners that plan to stay in their homes for the foreseeable future and want to get the most enjoyment and functionality out of living there. These homeowners typically aren’t as concerned, if at all, with getting a monetary return on their investment as their return is the enjoyment of the improvements. However, other homeowners, particularly those that may only be in their homes a couple of years or so before their next move, tend to focus more on making sure the remodeling they do will bring them a return on their investment to make it worthwhile. Granted, the return may be less than the cost but, after factoring in the enjoyment from the improvement the improvement may be worth it.

What are the remodeling projects that bring the best returns?

The U.S. population between 2019 and 2020 grew at the lowest rate in 120 years—just .35%, according to the U.S. Census Bureau. But low population growth didn’t stop many people from moving, as western and southern states saw influxes in population while California and New York saw the biggest drops.Stacker compiled a list of states that are sending the most people to Missouri using data from the U.S. Census Bureau. States are ranked by the number of people that moved to Missouri from the state in 2019.

The 2019 National Movers Study found that the states with the most inbound moves were Vermont, Idaho, Oregon, Arizona, and South Carolina. Keep reading to find out which states are sending the most people to Missouri.

How ‘smart’ can a smart home be if its locks can’t tell you who is coming and going and when they came and went? In my opinion, that’s not a very ‘smart’ house. Nowadays, we use our phones for much more than talking to other people. To name a few, we use them for directions, email, and paying for groceries. So why wouldn’t we use them to remotely lock and unlock our doors too?

From my previous articles you might remember that one of the primary requirements in a smart home is either smart temperature control or a smart security feature. A smart lock meets the security feature requirement and it’s one of the simplest additions to your house. Many of these can be installed using the standard pre-drilled holes that likely already exist in your doors. Usually, in under 25 minutes, you can go from fumbling around for the keys to your door automatically unlocking as you approach.

Have you ever been running a little late to an appointment and get 10 minutes down the road only to wonder if you locked your door? Yeah, me too, but with a smart lock, you could just get to the next stoplight and check your phone to verify the lock status. If you did forget, no worries—just tap the lock icon on the phone app and problem solved.

Another great feature of most smart locks is knowing who accesses the house and when. This can be done either through the assigned app or individual user codes. For peace of mind, you can track who comes and goes.

One of my favorite features is the autolocking function that can be tied to arming your security system. You no longer need to walk around and check all your doors because the system will just lock all the doors when you arm your alarm. Of course, you’ll need a security system for this feature, but some smart locks can be programmed to lock automatically at preset times throughout the day. If you have toddlers, this is a great feature. Mine love randomly unlocking doors and not telling me, so without that feature, the door would remain unlocked until I notice it.

Do you own an Airbnb? These locks are great for creating temporary access codes for each paying guest. Just like magic, once their reservation is up the code no longer works. Overall, smart locks are a great addition to modern lifestyles and they’re an affordable addition to virtually anyone’s home security. Plus, you don’t need an engineering degree to install one.

Interested in knowing MORE about Smart Home tech? Contact the only Smart Home Certified CRS agent in the Greater St. Louis area. *

*Based upon actual knowledge the author has at the time of publication”;

Interested in knowing MORE about Smart Home tech? Contact the only Smart Home Certified CRS agent in the Greater St. Louis area*.

*Based upon actual knowledge the author has at the time of publication

Mortgage interest rates were at 3.69% for a 30-year fixed-rate loan as of this past Thursday, February 10, 2022., according to Freddie Mac’s Primary Mortgage Market Survey®. As the chart below illustrates, mortgage interest rates hit a low of 2.77% in August of 2021 and have pretty much been trending upward since.

Within the last few days, there have been a lot of reports in the media projecting mortgage interest rates to go higher this year. A lot of it is based on the current inflation rates which are not good so if the economy and rate of inflation improve, so would mortgage rates but time will tell. Personally, as of today and subject to any new major disruptions, I think rates in 2022 will stay in the mid 3% range and climb to the upper 3’s, perhaps 3.9% but could very well go over 4% if the Federal Reserve raises rates as much as is currently rumored now.

According to Fannie Mae’s® Home Purchase Sentiment Index® (HPSI), 70% of consumers say it’s a bad time to buy a home while 25% feel it’s a good time to buy. As the chart below illustrates, this is the highest level reached for it not being a good time to buy in the 3-year period the chart covers. Actually, this is the highest level it’s reached since Fannie Mae began tracking the data in 2010.

Millennials are pessimistic about home buying…

The bottom chart also reflects the sentiment of consumers in the survey about buying a home now but is broken down by age group. This chart shows the net percentage of those saying it’s a “good time to buy” less those saying “it’s a bad time to buy”. The higher the line goes on the chart the more the good time to buy folks outweigh the bad time to buy. As you can see, the black line, which depicts consumers in the 35-44 age group is the lowest on the chart with a net of -68. This is the result of 83% of the consumers in this age group saying it is a bad time to buy and just 15% saying it’s a good time, resulting in a net of -68%.

Seniors have a better feeling about the market…

The red line depicts the sentiment of those 65 years and older and the net percentage there is -26%, so, while the percentage of people that feel now is not a good time to buy still outweighs the ones in this age group that think it is a good time, the resulting difference is about 40 points better than the millennial group.

There were 4,825 building permits issued for new single-family homes in the St Louis area during 2021 which is 9 more permits than were issued in 2020, according to the latest data from the Home Builders Association of St. Louis & Eastern Missouri (St Louis HBA). For the past few years, St Louis has experienced a strong seller’s market due to the low supply of homes for sale.

This demand certainly seems to be something that would encourage builders to increase the number of homes being built significantly. However, there are many challenges facing St Louis builders today that prevents this. The challenges include a shortage of developed lots, or even ground in areas of demand, as well as increased construction costs, a result of regulatory issues, material prices and construction worker’s wages. If the builder can deal with the increased prices, then there are supply chain issues and labor shortages to deal with as well. Selling new homes is pretty easy today, the challenge is developing them.

Most anyone that is interested in buying or selling a home is pretty much aware of two things: there is a low inventory of homes for sale and prices have increased a fair amount as a result. That part is likely largely a result of basic economics related to supply and demand. When the demand is greater than the supply, prices will increase. In St Louis, home prices have done just that. As the chart below (exclusively available from MORE, REALTORS®) illustrates, the median price of homes sold in January 2020 was $221, 200 and in January 2021 was $245,000, an increase of 10.8%.

Interest rates are the other part of the equation with regard to the “cost” of a home…

Since the overwhelming majority of home buyers that purchase a typical home in St Louis do so utilizing a mortgage or home loan, the interest rate on that home loan has a direct impact on what that home “costs” the homeowner in terms of the monthly payment. When buyers get pre-approved for a home loan, as well as consider how much they can afford to or want to, spend on a home, it all pretty much usually starts with the house payment. Therefore, we can’t underestimate the impact interest rates can have on home prices.

As the mortgage interest rate chart below shows, the average interest rate on a 30-year conforming conventional home loan in January 2021 was 2.811% and today has increased to 3.744%.

The change in the “cost” of a typical St Louis home in the past year…

So, if we look at the increase in the price of a typical St Louis home and then factor in the increase in the interest rates we find that the actual “cost” of a typical St Louis home (in terms of house payment) increased 25% n the past year. To keep things simple, I based this on a loan amount of 90% of the purchase price so the cost will vary depending upon downpayment of course and I’m only computing principal and interest so I’m not including escrows for property taxes or homeowners insurance.

Typical payment on a typical St Louis home January 2021 – $ 805.00

Typical payment on a typical St Louis home January 2022 – $ 1,009.00

Is it too late to buy since the cost has increased so much?

Today, thanks to many apps and access to information, all consumers have ready and easy access to their FICO (credit) score. Anyone thinking of buying a home no doubt knows their credit score will come into play in terms of qualifying for a mortgage but just how significant is your credit score? Is there really that much difference between a 670 and 700 credit score, or between a 700 and 741 score? Well, when it comes to mortgage rates, it does make a difference!

A 670 FICO vs a 741 FICO will run up the typical cost of St Louis home over $17,000 over the life of your loan!

For example, as the table below illustrates, the median interest rate for a mortgage for a person in St Louis (borrowing over 80% of purchase price) with a FICO score of less than 680 is 3.962% versus an interest rate of 3.611% for someone with a FICO score above 740. The median price of homes sold in St Louis during the past 30 days was $245,055. So, to make it simple, if we assume that for the loan amount a person with a 679 score would be looking at a house payment of $1,153 per month (principal and interest) while someone with a 741 credit score would be looking at a payment of $1,104 or $49 per month less. That may not sound like much, but over the 30-year life of the mortgage that means the person with the lower credit score will pay $17,640 more in interest than the borrower with the higher score. Or, to look at it a different way, for the same payment of $1,153 that the lower score borrower will pay for a $245,055 home, the borrower with the higher score can buy a home that costs $255,823.

Mortgage interest rates were at 3.667% for a 30-year fixed-rate loan as of this past Thursday, January 13, 2022. As the chart below illustrates, after dipping slightly the week prior, the rates this most recent week hit the highest level in over a year.

Mortgage rates for an FHA mortgage also hit the highest level in over a year too with rates hitting 3.743%.

Do you like inconvenience? Spending more money than needed? Do you like things to be more difficult than needed? Do you like not knowing how much energy you use and when you use it most? Do you desire suboptimal temperature control? If you answered ‘no’ to these questions then whether you knew it or not, you’re already convinced that a Smart Thermostat is worth a couple of hundred bucks to you.

One of the primary requirements in a ‘Smart Home’ is either smart temperature control or a smart security feature. Of these two, the one to likely pay for itself first is the smart thermostat. It may sound a little creepy but most smart thermostats are self-learning which means they adjust the temperature based on your habits and schedules. The simplest example is that they know when you are sleeping, and they know when you’re awake. They know when you’re away from the house too, and because of this intuitiveness, it can adjust the temperature accordingly. How does it know these things? Glad you asked. These types of thermostats use a combination of scheduling, geofencing, and motion detection to know how to adjust.

As the charts below illustrate, at the beginning of this year, mortgage interest rates for a 30-year conforming conventional loan were at 2.771%, FHA loans were at 2.703%, and VA loans were at 2.372%. As of yesterday, those rates have increased to 3.357%, 3.468%, and 3.101% respectively.

While conforming 30-year conventional loans have seen an increase of 21% in rates (from 2.771% to 3.357%), FHA loans have seen an increase of 28% (from 2.703% to 3.468%) and VA loans have seen an increase of 30% (from 2.372% to 3.101%).

What does this mean in terms of the cost of a home?

To make the comparison simple, I’ll just base my comparison on the price of a “typical” home in the St Louis 5-county core market using the median price of homes sold in October which was $234,900. Downpayments will vary based upon loan type from no downpayment being required on a VA loan, to a minimum of 3% on a conventional and 3.5% on an FHA but based upon a loan amount equal to the median price of $234,900, below are the differences in the monthly payment on that amount by loan type from the beginning of this year until now:

Conventional – $948 to $1,023

FHA – $939 to $1,038

VA – $898 to $990

If we factor in the increase in home prices, it gets worse.

In the “to add insult to injury” category, home prices have increased significantly since January as well, In January the median price was $215,000, so between then and October the median price of a St Louis home increased 9.2%. With the interest rates increasing at the same time the cost of a typical St Louis home increased fairly significantly as shown below:

Conventional – $867 to $1,023 (+18%)

FHA – $859 to $1,038 (+21%)

VA – $821 to $990 (+21%)

The moral of the story…don’t wait to buy.

While I certainly can’t predict the future, especially given all the uncertainty in our economy with inflation, employment issues, etc, if I were in the market to buy a home I don’t think I would wait “until things get better”. The reason for my opinion is, as I’ve illustrated here, the true “cost” of a home (assuming you are not paying cash for it) is a combination of price and interest rate. So, even if home prices see an adjustment or the seasonal dip we often see during winter if interest rates continue to rise, is the higher cost of borrowing going to offset the lower price? I think that is a possibility. Or, the flip side, if interest rates go down but then prices go up, is the savings in lower rates lost?

To benefit from waiting, in terms of the cost of the home, we would need interest rates to stay the same, or decline and home prices to decline or interest rates to drop and home prices stay the same. Right now I don’t see either of the two aforementioned scenarios likely to happen.

Simply put, a Smart Home means your home has a control system that connects with your various appliances, systems, and features to automate specific tasks and is typically remotely controlled. The real estate industry, in conjunction with CNET, accepted definition is:

“A home that is equipped with network-connected products (aka “smart products,” connected via Wi-Fi, Bluetooth, or similar protocols) for controlling, automating, and optimizing functions such as temperature, lighting, security, safety, or entertainment, either remotely by a phone, tablet, computer, or a separate system within the home itself.”

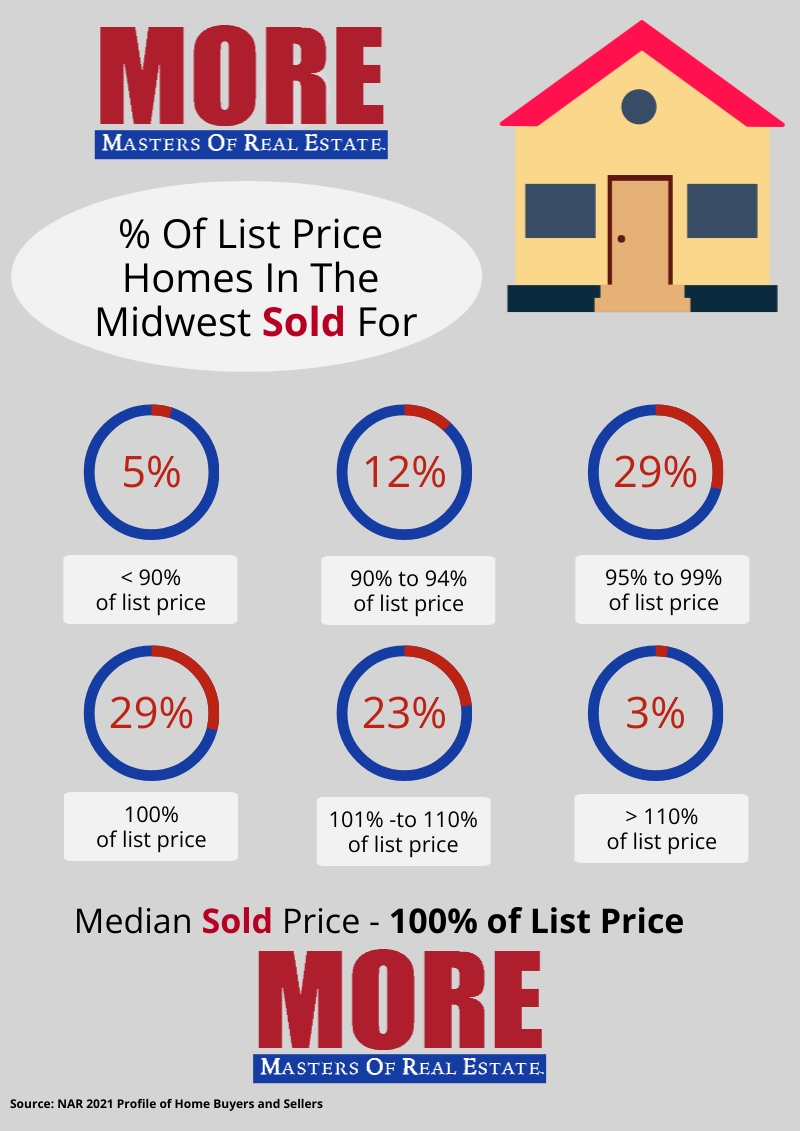

Last week I published an infographic in an article illustrating that 65% of the homes sold in St Louis sold at or above the list price. As the infographic below shows, this is a significantly higher percentage than was experienced in the midwest region as a whole where 55% of the homes sold at or above full price.

Two-thirds of the homes sold in the St Louis 5-County core market (St Louis city and the counties of St Louis, St Charles, Jefferson, and Franklin) during October sold for the asking price or above. As the infographic below shows (exclusively available from MORE, REALTORS®) there were 2,888 homes sold during October in the St Louis 5-County core market with 65% of them selling at the list price or above. One thing to remember about home prices though, and something you won’t hear from too many people reporting prices, is that not all sold prices are the “real” price.

Missouri Online Real Estate, Inc. 3636 South Geyer Road - Suite 100, St Louis, MO 63127 314-414-6000 - Licensed Real Estate Broker in Missouri

The owner and authors this site are providing the information on this web site for general informational purposes only and make no representations, warranties (expressed or implied) or guarantees of any kind whatsoever, as to the accuracy or completeness of any information on this site or of any information found by following any link on this site. Furthermore, the owner and authors of this site will not be liable in any manner whatsoever for any errors or omissions in information on this site, nor for the availability of this information. Additionally the owner and authors of this site will not be liable for for any losses, injuries or damages in any way from the display or use of this information or as the result of following external links displayed on this site, or by responding to advertisements displayed, or contained, on this site

In using this site, users acknowledge and agree that the information on this site does not constitute the provision of legal advice, tax advice, accounting services, investment advice, or professional consulting of any kind nor should it be construed as such. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal, or other competent advisers. Before making any decision or taking any action on this information, you should consult a qualified professional adviser to whom you have provided all of the facts applicable to your particular situation or question. None of the tax information on this web site is intended to be used nor can it be used by any taxpayer, for the purpose of avoiding penalties that may be imposed on the taxpayer.

All of the information on this site is provided as is, with no assurance or guarantee of completeness, accuracy, or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability, and fitness for a particular purpose.

This site contains external links to other sites not owned or controlled by the owner of this site, therefore the owner of this site does not control or guarantee in any manner the accuracy or relevancy of any information obtained through following such links. Links contained on this site are for users convenience and users should exercise extreme caution when following links. Including a link on this site does not constitute an endorsement of the site linked to or any views or opinions expressed on the site, products or services offered on outside sites or the companies or organizations that own and operate outside sites.

This site may accept payment for advertising, for displaying advertisements, through affiliate relationships with companies or may receive referral fees or commissions from companies as a result of recommending or referring people to a website. This site may also accept free product samples, free services, gift cards or cash to review a product or service. All paid and sponsored content may not always be identified as such. Any product claim, quote or other representation about a product or service should be verified with the manufacturer or provider.